Agricultural robots are a natural next step in the technology progression of agricultural machinery. In fact, these are special times in the development of agricultural robots because the cost of computing and data acquisition has dramatically fallen over the decades, finally enabling robots that transform many aspects of agriculture.

Indeed, the IDTechEx Research report Agricultural Robots and Drones 2017-2027: Technologies, Markets, Players finds that the agricultural robotic and drones market will nearly reach $10bn by as early as 2022. Here, in many cases such as tractors, we only count the value of the automation system and not the entire vehicle.

Robots and autonomous systems have been quietly transforming farming for years. In fact, farming is still today the leading and earliest adopter of manned autonomous navigation vehicles. Here technology is already advancing further here to take the driver completely out of the equation, thereby helping completely turn our long-held vision of agricultural machinery upside down.

This is because unmanned autonomous farm vehicles can enable a transition away from one large, heavy, and fast vehicle towards swarms of small, light and slow robots. Here, start-ups lead the way as large existing vehicle manufacturers are afraid of cannibalising their own core products.

Start-ups are re-defining agricultural machinery

Research institutes, start-ups, or early stage companies are now developing robots and autonomous systems to address challenges in all aspects of agricultural. This, for example, includes strawberry picking, lettuce thinning, weeding, seed planting, feed pushing, fresh fruit harvesting, milking, data collection/mapping/monitoring, bin collection, and so on.

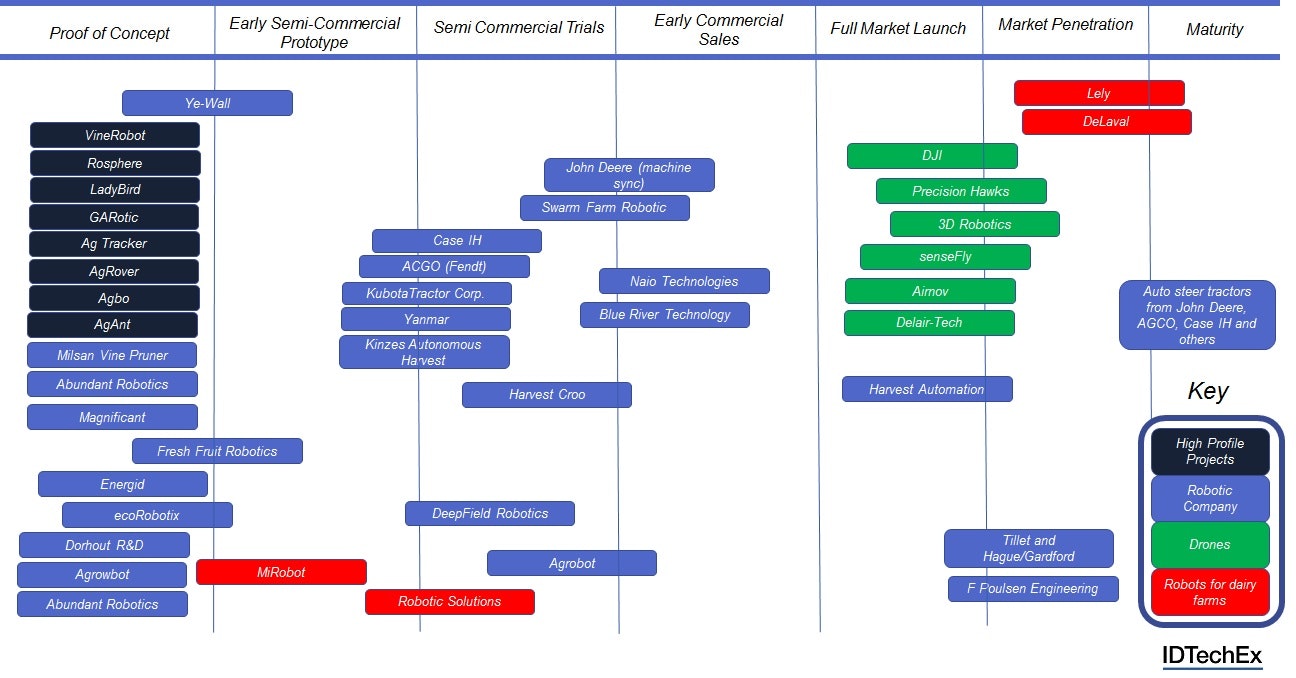

The schematic below shows the degree of commercialisation of various companies active in agricultural robotics and drones. Here, it is observed that companies active in, for example, robotic milking products are already in the late market penetration/early maturity phase whilst drones (hardware and data processing) are in full the market launch/early market penetration phase.

In contrast, start-ups focusing on small unmanned autonomous farm vehicles are in the semi-commercial trail or in the early commercial sales phase. Similarly, companies focusing on larger unmanned autonomous tractors are also in the semi-commercial trial phase, whilst companies developing fresh fruit picking robots (arms, end effectors, vision, and so on) are at an even earlier stage, often having only just demonstrated their first prototypes or proof-of-concepts. The chart below is by no means comprehensive and more companies are covered in the report Agricultural Robots and Drones 2017-2027: Technologies, Markets, Players

Market readiness of different companies and high-profile projects in agricultural robotics and drones. This is not a comprehensive chart. For a more complete analysis please refer to Agricultural Robots and Drones 2017-2027: Technologies, Markets, Players

Value chain of agriculture: change is well underway

The interest in agricultural robotic is booming. This growth is rising in tandem with activities around the introduction of sensors, data analytics and optimal management platforms into farming. This trend can be viewed within the context of the bigger Internet of Things theme and is expected to alter the traditional value chain of agricultural, hugely increasing the value captured by sensing, data processing and robotic/autonomous systems.

Change is well underway. Inevitably, farmer conservatism will slow down the adoption, covering these developments into a slow evolutions, but ultimately farmer pragmatism will embrace these changes once they become more proven and reliable. In the meantime, expect to see start-up adopt the RaaS (Robotic as a Service) business model to reduce the risk to the farm by minimizing their upfront capital commitments, decreasing changes to the current operational methods, and keeping intact their cost models (e.g., $ per harvested box).

Agricultural Robots and Drones 2017-2027

This report is focused on agricultural robots and drones. It analyses how robotic market and technology developments will change the business of agriculture, enabling ultra-precision farming and helping address key global challenges.

It provides granular ten-year segmented market forecasts for 14 categories. It offers provides detailed technology assessment covering all the key technological components such as vision sensors, LIDARs, novel end-effectors, and hyper/multi-spectral sensors, and so on. It also includes more than 20 interview-based full company profiles with detailed SWOT analysis, 40 company profiles without SWOT analysis, and summarized coverage of the works of more than 80 companies/research group.

For more see www.IDTechEx.com/agri