Industrial robotic arm sales have tended to be cyclical in the past. The last major dip in sales came on 2009 following the financial crises when the year-on-year unit sales crashed by some 47%. The market rapidly recovered and embarked on a sustained growth cycle. Indeed, by 2014, the unit sales had doubled compared to the pre-crises level. This boom period shows no signs of immediate slow down.

In this article, we will explore the basis of this growth supercycle and consider the short- and long-term future of industrial robotic arm sales. We will also discuss the impact of other trends such as the rise of collaborative robotic arms, the emergence of new players and applications for surgical arms, and the progress in other uses of robotic arms such as dairy farming. For more information, we refer you to the IDTechEx Research report New Robotics and Drones 2018-2038: Technologies, Forecasts, Players.

In this comprehensive report IDTechEx Research will consider the past, present and the future of robotic and drone technologies. We will provide twenty-year forecasts in value and units numbers for 46 categories. This report provides detailed technology analysis, assessing the trends in performance and price of key enabling hardware and software technologies whilst considering likely technology development roadmaps. We will also profile key companies and innovative entities working on new robotics and drones.

This report is unique in its depth and breadth. This is because it examines traditional (old) as well emerging (new) robotics. Indeed, we believe that a major transformation is taking place with robots becoming uncaged, mobile, collaborative and increasingly intelligent and dexterous. This report is designed to cover the key trends shaping the future of traditional (old) robots, whilst also offering a detailed and comprehensive analysis of emerging robotic applications. For more information visit New Robotics and Drones 2018-2038: Technologies, Forecasts, Players.

China is already the largest robot purchaser

The first commercial installation of a robotic arm was in 1951. This was a simple arm able to do basic pick-and-place. There was little change in technology until 1968 when the first 'programmable' industrial robot came to market. The first 6-axis robotic arm came to market in 1977. The pace of innovation was therefore relatively slow within the first two decade of robotic arm development.

The industry has come a long way since then. Today, more than 2M industrial robot units are installed worldwide. Now, rows of industrial robotic arms carry out high volume production in many industries including automotive, material handling, electronics, metal/chemical production, and even, increasingly, food processing. The robotic arms themselves come in a variety of sizes and types (DELTA, Articulated, Cartesian, SCARA, etc).

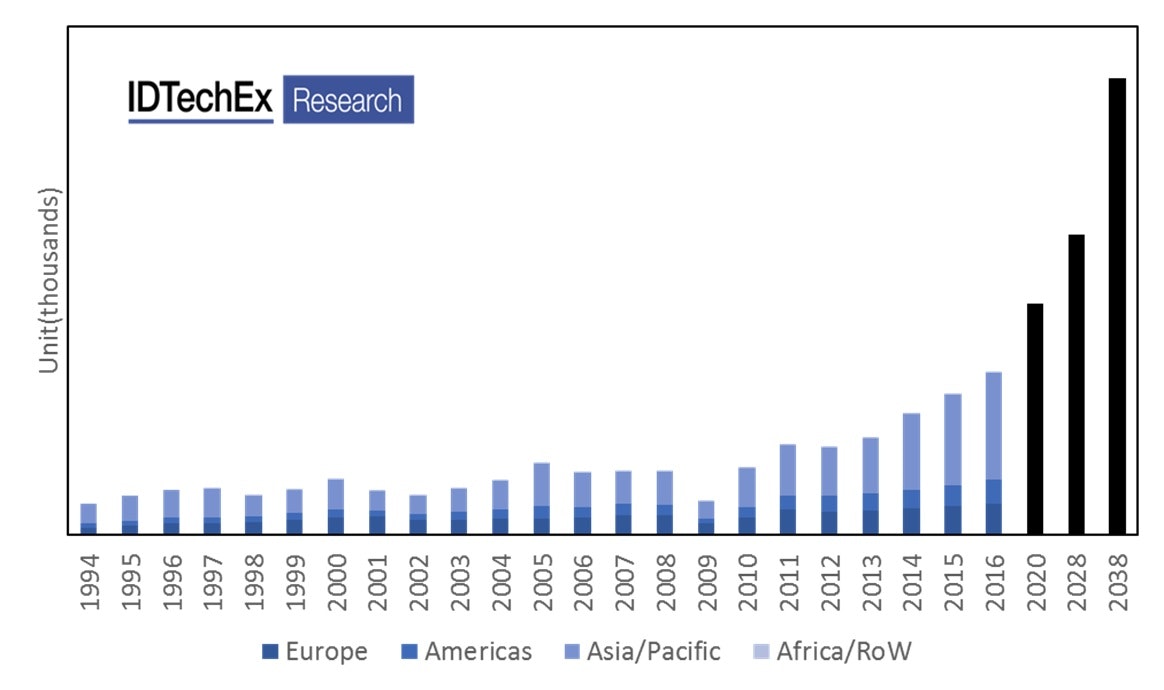

The chart below traces the development of industrial robotic arms in unit sales (for actual values see New Robotics and Drones 2018-2038: Technologies, Forecasts, Players). First note that past market behaviour has been cyclic, characterised by periods of booms and bust. This is not atypical as spending on automation is linked to CapEx spending in major industries that are in turn linked to the health of global economy.

The chart below shows that Asia has been- by far- the leading adopter of industrial robotic arms. This is no surprise as China, Japan and Korea are major manufacturing territories in industry after industry. Europe and America are also major powerhouses whilst the rest of the world follows by some distance.

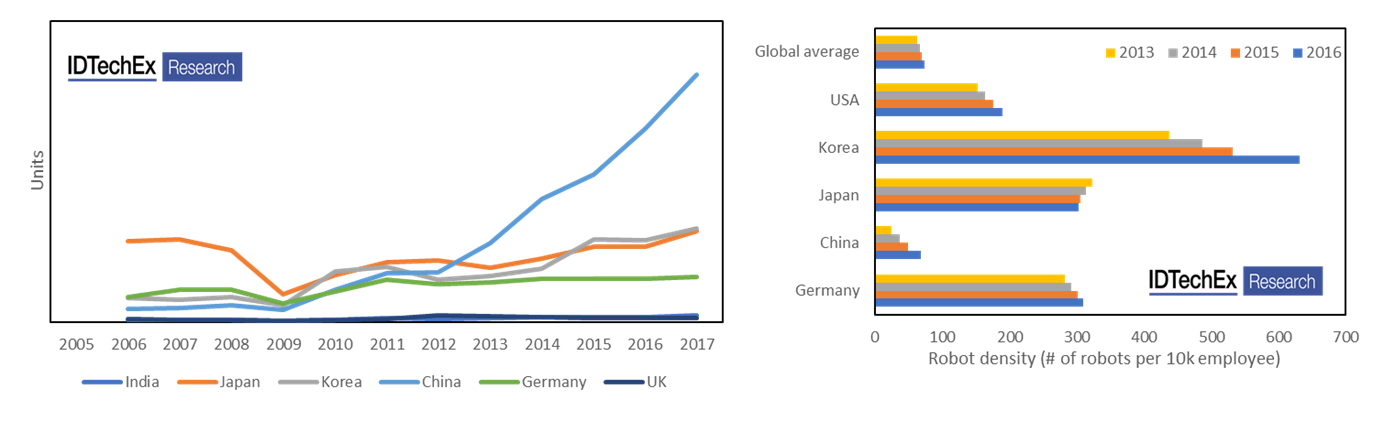

The market is now in a period of sustained growth (a growth supercycle). This is largely thanks to developments in Asia and more specifically China. The chart below (left) shows unit sales by territory (for detailed figures consult New Robotics and Drones 2018-2038: Technologies, Forecasts, Players). Here we will see that countries such as India are laggards reflecting the state of their economy. Interestingly, UK is also a laggard compared to other leading European nations, reflecting the fact that services now dominate its economy. In Europe, Germany is the leading purchaser of robots.

The main activity however is in Asia. For long, Japan has been a major adopter for robotic technology. Indeed, Japan started its rapid automation spending spree from 1997. Today, it boasts great technical know-how and many leading global suppliers. Korea has also invested heavily in automation, but in more recent times.

Figure:1 annual sales of industrial robotic arms by territory from 1994 to 2038. The data until 2016 is historical data whilst the bars shown in black are our future projections. For more details and the numbers please refer to the IDTechEx Research report New Robotics and Drones 2018-2038: Technologies, Forecasts, Players.

China, however, was traditionally a massively under performing adopter of robotic technology, especially considering its population. It only joined the fray from 2000 and accelerated its activities from 2012. Interestingly, China became the largest purchaser of robots in 2012-2013, surpassing other leading nations such as Japan and Korea.

It is this rapid rise of China that has pushed the market into its growth supercycle. Chinese spending in the past had put the commodities market globally into a growth supercycle phase and now appears to be doing the same to the robotic industry.

The question however is how far can this go? To answer this question, it is instructive to compare the robotic density of China (number of robots per 10k employees) with the rest of the word. This is shown below. We can observe that China was below the world average by as late as the end of 2016. It was also far below the robotic density level of other major industrial countries such as Japan, Korea, Germany and USA. This suggests that we are only at the beginning of the beginning of the long-term rise of Chinese demand.

Figure 2: (Left) sales of industrial robots by country. (Right) robotic density of different countries at different years. For more details and for the numbers please refer to the IDTechEx Research report New Robotics and Drones 2018-2038: Technologies, Forecasts, Players.

To develop our projections, we modelled the future behaviour of China on the historical behaviour of Japan. Indeed, we demonstrate that the rise of automation in China since 2008 closely mirrors developments in Japan when it started to rapidly automate from 1976 onwards. Furthermore, China also suffers from an unfavourable demographic with its working population already having peaked. This, together with China also seeking to compete on quality, will necessitate and sustain the adoption of further automation technologies. We model the behaviour of the rest of world on the long-term growth patterns of the past. This approach enables us to develop short-term, medium-term and long-term projections for the market for industrial robotic arms, in unit numbers as well as in market value. These figures are included in our report.

The total aggregate results are shown in black in figure 1. Here, we can observe that the market is on an upward trajectory in the future. Our model suggests that there will continue to be periods of boom and bust, as is intrinsic to industries linked to CapEx spending. The general direction of travel however will remain upwards barring a major unforeseen event. Asia will remain the leading territory and China will increasingly support and develop a local ecosystem of suppliers who will, in time, rise to challenge others not just on cost but also on performance. This will be an interesting development to watch.

Collaborative arms: everyone has followed suit

Collaborative robotic arms are opening automation opportunities in tasks where humans are also involved or are in close proximity. Furthermore, they are also opening automation opportunities to small- to medium-sized business.

The market for collaborative robotic has been experiencing high year-on-year growth. This has enticed almost every major robotic company to add a collaborative series to its portfolio. This means that now, following the success of the early pioneers, the market enjoys having multiple suppliers and products, covering a wide spectrum of price and performance levels (degree of freedom, repeatability, reach, payload, speed, ease of programming, etc).

A key feature of collaborative robots is safety since they are in proximity with human worker. In general, this has meant that these robots deal with smaller payloads and generally minimize their momentum. This is to ensure that no pain or injury is caused upon contact. Furthermore, the robots are equipped with sensors to foresee and/or detect collision. Some have cameras seeking to measure a safe distance whilst many others have torque sensors built into their joint motors or benefit from sensor skins.

In this report we benchmark the numerous collaborative robots on the market today. We then highlight several key existing and emerging applications for such robotic arms before assessing the various types degrees of collaboration, the various forms of safety measures, and the status of the legislation and standards regulating the deployment of collaborative robotic arms. Finally, we provide our short- as well as long-term market projections.

Other sizable applications (surgical and dairy farming)

There are two other sizeable applications of robotic arms that we cover in our report: surgical robots and milking robots.

The basic idea in robotic assisted surgery is that the surgeon can remotely and digitally control and monitor robotic arms that perform a function (ablation, measurement, insertion, etc.) on the patient. These can be also considered as collaborative robots since they are in contact with the patient.

These precision robots (0.01mm) can help level the playing field of surgical skills and extend the working life of surgeons. This is because they can essentially remove the adverse effects of hand tremors. These robots can also enable access to various body parts in ways that were previously impossible.

These robots are becoming increasingly better equipped with better sensing tools (e.g., imaging). They will also incorporate more data analytic capabilities into the platform to further aide humans in developing and executing surgical strategies.

Robotic assisted surgery has been a major commercial reality for more than a decade. In 2017 alone, more than 800k procedures were expected to be conducted using surgical robots in urology, gynaecology, general surgery and others.

The incumbent supplier currently dominates the market, enjoying healthy margins from the sales of its robotic systems, instruments and support services. Others are now however seeking to challenge this dominance. Several well-capitalized companies have brought products onto the market and received approvals. They are generally still without significant sales. However, this is only the beginning for them. Other firms are seeking to expand the use of robots into new surgical operations such as orthopaedic or those involving precise catheter movement manipulation, whilst spreading the use of surgical robots to new territories beyond current strongholds, e.g., USA.

Dairy farming is also already a commercial success story. Here, robotic arms (part of the larger automation system and placed inside a parlour) help automate the milking process. These rugged robotic arms are equipped with a suction cup and a simple laser-based localization tool which estimate the distance by calculating the amount that a pattern of well-shaped laser dots is stretched when incident upon the target. This technology is now commonplace, having demonstrated its utility in boosting productivity and sales are fast increasing. This is a multi-billion dollar industry that often receives little attention.

Note that we also briefly provide information on 3D printing machines for the sake of completeness. These are often essentially a robotic (often Cartesian but some Delta robots are used too) apparatus that manoeuvres an extrusion or a laser head. We provide forecasts for both consumer (where the hype was) and professional (where the money is and will be) 3D printers. For detailed sectoral and technological analysis however we suggest you see our dedicated reports on various aspects of 3D printing.

For further information please refer to New Robotics and Drones 2018-2038: Technologies, Forecasts, Players. Here we provide short-, medium- and long-term forecasts for 46 robot and drone market categories, covering both traditional and emerging robotic and drone technologies. More specifically, we cover robotic arms( industrial, collaborative, surgical 3D printing, dairy farming); autonomous robotic cleaning and mowing ( home, commercial, pool cleaners and lawn mowers), autonomous commercial robots (retail and security) agricultural robots (level 3, 4, and 5 autonomous tractors, agrobots, intelligent robotic implements, fresh fruit harvesting, etc.), logistics (AGV/AGC, AMRs, forklifts, last mile delivery, long-haul, trucks, etc.), drones (consumer, prosumer and professional), and beyond.

See https://www.IDTechEx.com/robotics for more.