Old (existing) robotics is growing. In fact, it is arguably in the midst of a growth supercycle. As we recently wrote, this is largely thanks to demand in China. Indeed, China is already the leading purchaser of robots despite still having a below average robotic density and thus extensive room for future growth.

In parallel to this, the world of robotics is being fundamentally transformed along three primary axes: increased collaboration, increased autonomous mobility and increased intelligence. This change will shape the future of automation and thus robotics.

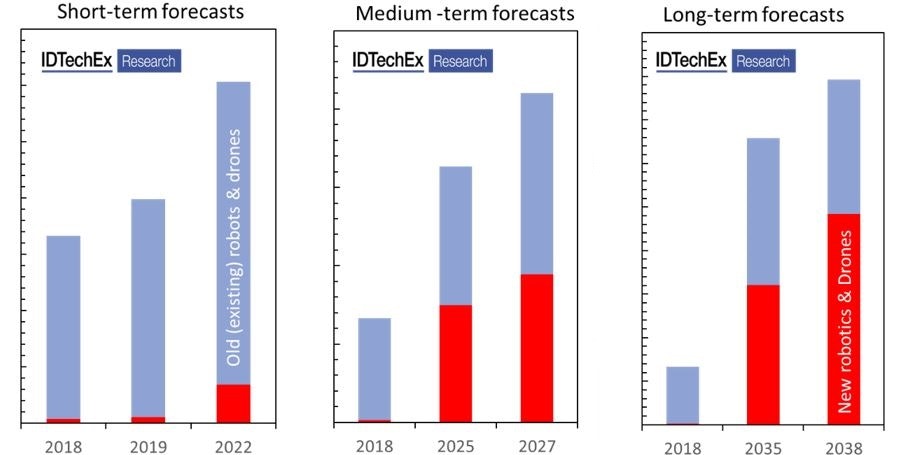

Indeed, as shown below, our forecasts, published in New Robotics and Drones 2018-2038: Technologies, Forecasts, Players, suggest that new robotics will grow to represent more than half the market around 2028/29 despite starting from low base (2% in 2018). This is even more exciting when we consider that old (existing or traditional) robotics is also rapidly growing itself.

In this article, we will describe this upcoming confirmation. This analysis is drawn from our report New Robotics and Drones 2018-2038: Technologies, Forecasts, Players, which assesses more than 6 categories of existing and emerging robotics and drones. In this report, we provide technology roadmaps, application analysis, and profile/overview of key innovators and players. We also offer detailed quantitative 20-year market forecasts, covering the short-, the medium- and the long-term likely developments within this field.

The world of robotics is changing. New robotics will rise from a nascent base to dominate the market in the medium- as well as the long-term. This rise will represent an enormous transformation in automation technologies, affecting numerous studies. This will create numerous opportunities but also threats. Note that for our aggregate value for existing robots in our report we include industrial robotic arms, surgical robotic arms, milking robots, 3D printers, partially autonomous tractors (level 3 and 4), AGV/ACGs, robotic vacuum cleaner and lawn mower and other similar categories. For new robotics, we cover the rest of the 46 categories. Note that on-road autonomous passenger cars and mining vehicles are excluded from this figure. For more details consult New Robotics and Drones 2018-2038: Technologies, Forecasts, Players

Old (existing) robotics: already more diverse than often assumed

Existing robotics is typically associated with stationary robotic arms carrying out a precise repetitive task in a robot-only industrial setting. This is of course the primary market. We described its key dynamics in a previous article recently. Here, we will instead focus some of the diversify of existing robots outside industrial robotic arms.

Old (or existing) robotics is more diverse than at first meets the eye. Within stationary robotic arms we have many sectors beyond industrial use cases: medical, collaborative, milking, etc. Within automated or autonomous robots, we have automated guided vehicles/carts, tractors (level 3 and 4), robotic cleaners and lawn mowers, and several other technologies. For airborne robots, we have line-of-sight consumer drones. Photos above, in no particular order, are from Kawasaki, Mitsubishi, John Deere, Intuitive Surgical, Amazon, 3DR, Kuka, Xiaomi, Parrot, Yuneec, Garford, Maytronics, Neato, Lely, Bosch, Honda, Walkera, SSI Schafer, etc. For more details please refer to New Robotics and Drones 2018-2038: Technologies, Forecasts, Players.

Stationary robotic arms beyond industrial uses: First let's remain focused on robotic arms. We have 3D printers, surgical robots and milking robots. 3D printers are mainly (though not entirely) based on a Cartesian robotic design. The consumer end of the market was hyped but is now facing commoditization and even sales declines. The professional end however is set to continue its growth as 3D printers become more productive.

Surgical robots are also already a significant success story mainly in USA and Europe. A single company today dominates the market, earning healthy margins. The short to medium term trends in this market will thus be (a) the rise of challenger companies seeking to share in the incumbent's growing success and (b) the attempt to expand robot use into new procedures and territories.

Milking robots are also a significant commercial success already. We have written on this topic before and refer to our report page for more details - Agricultural Robots and Drones 2018-2038: Technologies, Markets and Players.

Automated or autonomous existing robots: Not all existing robots are stationary. Automated infrastructure-dependent automated guided vehicles and carts (AGVs and AGCs) have been in use since 1950s in industrial and warehouse settings. The market for these today is fragmented by supplier and use case. The market size, we forecast, will remain steady in the immediate future.

However, change is coming here. Indeed, our roadmap suggests infrastructure-independent autonomous (vs. automated) mobile robots will increasingly take over, slowly pushing rigid AGVs and AGVs towards obsolescence (note: Kiva-like grid-based AGCs used in warehouses will remain a bright spot).

More autonomous (vs. automated navigation) robots have also been in commercial mode for years. Take the home environment as an example. Here we have had robotic cleaning for years. This is in fact already a billion-dollar market. First, these robots randomly roamed around room. Next, the became equipped with more intelligent structured path planning. And now they are being positioned as the centre of the emerging smart home ecosystem.

The market trends now are (a) increased commoditization, (b) attempts to supress competition through IP blocking; and (c) growth in Asia. The robots will also grow in size, in power, and in productivity, opening the door to professional and commercial cleaning applications.

Our definition of existing robotics in this report also includes partially autonomous (level 3 and 4) tractors. Indeed, as we have previously written, agriculture is the leading adopter for autonomous mobility technology. For sake of brevity we will not cover the details but refer to Agricultural Robots and Drones 2018-2038: Technologies, Markets and Players.

New robotics: more collaborative, more autonomous, and more intelligent

New robots will be more collaborative, more autonomous, and more intelligent. In the rest of this article we will explore these developments. For a detailed analysis see New Robotics and Drones 2018-2038: Technologies, Forecasts, Players.

New (or emerging) robotic and drones include a diverse array of technologies and use cases. Various examples are shown above. In general, new robots will be more autonomous, more collaborative and more intelligence. The robots shown above are, in no particular order, from Avidbot, Metral Labs, Pal Robotic, Starship, Simbe, AliBaba, Yamaha, ZipLine, Blue River Technologies (now John Deere), Bossa Nova, RowBot, FF Robotics, Fellow Robot, Keonn Technologies, MiR, InVia Robotics, Lely, EarthSense, AGCO, 4D Retail, RFSpot, Knighstscope, IAM Robot, Bosch, Automation Solutions, GreyOrange, SMP Robotic, Harvest Croo, Colbalt, Sensense, Gamma2Robotics, TwinWheels, Sharp, Ahteon, LG, Savioke, Otto, Dispath, etc. For more details please refer to New Robotics and Drones 2018-2038: Technologies, Forecasts, Players

Increasing human-robot collaboration: today most robots operate on robot only zones. Industrial robotic arms are caged off, grid-based goods-to-person warehouse AGCs shuttle around in exclusively robot areas, and traditional AGVs/AGVs are kept strictly within their well-defined guidance path.

In contrast, new robots will increasingly share the environment with humans. Collaborative arms will be deployed alongside humans or in hybrid arrangements. Here, the robots will be endowed with multiple sensors to avoid contact, and the robot momentum and payload will be kept low to ensure no harm even if impact occurs. These robots are opening new tasks to automation and opening automation to SMEs. Every major robotic company now has a collaborative arm. We forecast this sector to continue its strong growth.

AGVs and AGCs are also becoming more autonomous. As a result, they will increasingly diffuse outside the confines of separated zones in industrial/warehouse zones into day-to-day spaces such as shopping malls, offices, parking lots, roadside pedestrian pavements, hospitals, airports, and so on. This will be a dramatic change in that it can make robot an integral part of our regular daily experiences.

Increasing autonomous mobility: Today most (not all) robots are stationary, follow a rigid guidance path, or limited manned autonomy (level 3 or 4). In the future, robots will have unmanned autonomy. This will have profound consequences for many industries.

Let's consider several examples. In warehouses and industrial sites, AGV/AGCs will slowly give way to autonomous mobile robots (AMRs). Here, the driver will be enhanced versatility of AMRs and their lower installation time.

Autonomous mobility technology will also penetrate industrial vehicle industries (forklifts and tugs), enabling equipment markers to partially capture the wage bill that is annually spent on human-provided driving services. Indeed, we forecast, that despite the current conservatism of some major forklift companies, autonomous forklifts will emerge from 2022/2023 onwards, ultimately growing to represent 70% of the annual in 2037.

In delivery, last mile robots are being developed to address its inherent productivity challenge. Here, the key success is in unmanned autonomy. This is because these autonomous robots can achieve higher productivity and cost competitiveness at the level of the fleet even if each individual robot is slow and small. The primary reason is that autonomous mobility technology largely eliminates the driver's wage bill overhead per unit.

These last mile delivery robots are currently being trialled around the world. Today, there are most restricted to structured or uncongested outdoor environments like campuses. In the future, and with more experience, they will become more adept at navigating more complex environments, thus increasingly entering more diverse public spaces.

The same trend is taking place in sector after sector. Indeed, as robots improve their autonomous mobility technology, they are being deployed as outdoor and indoor security robots, retail assistance and stock keeping robots, hospital robots, hotel delivery robots, and so on. Even in agriculture, unmanned autonomy is giving rise to fleets of slow, light robots replacing a few fast and heavy tractors.

Our technology roadmap and forecasts suggest that these AMRs will become commonplace. In a similar fashion as the consumer drone industry, we foresee that the hardware platform will become modular and commoditized. One or a few winners will emerge supplying the hardware in volume for use in AMRs in different sectors. The supply of the software platform can also be consolidated with few players developing a software platform akin to an autonomous mobility operating system for robots.

There will however always remain ample opportunity to customize the software and to offer robot-enabled services. These will not be readily commoditized because the end use market is fragmented, and each sector will have its own peculiarities.

It might be interesting to note that increased autonomy will not be limited to robots. Drones will also become increasingly autonomous. This will require the sensor per drone to increase. Indeed, drones have already progressed from just a remote-control communication link towards flight stabilization using various IMUs, towards waypoint following using GPS, and towards object avoidance using cameras and ultrasound sensors. The legislation will also finally adapt, enabling beyond line of sight drone navigation.

Increasing intelligence: robots traditionally perform repetitive tasks in defined environments. They are given specific and explicit instructions (script or code) to follow. This is all changing. Indeed, new robots are essentially physical embodiment of artificial intelligence (AI) and are thus driven by progress in the AI field.

In particular, deep learning with data and computing power (GPUs) as its fuel is driving the field forward. This technique is enabling robots to learn specific tasks that were previously considered too challenging to script (or code). The improvement is in fact enabling robots to encroach on basic low-skilled areas in which humans were generally assumed to have a comparative advantage: grasping, recognizing, and speaking. The current success rate of robots suggests that humans will not forever hold onto these advantages.

Let us consider some examples. In warehousing, mobile robots essentially act as transporters whilst humans still do the picking. This will start to change within our forecast period. Already, deep learning has enabled robotic grasping to exceed 93% success rate when grasping novel irregular objects, and already companies are seeking to capitalize on this progress. In the short, they will focus on regularly box-like items. In the future, with experience and data, they will shift towards general mobile picking in many industries even off a mobile platform.

In agriculture, AI is enabling the traditional mechanical tractor-pulled implement to become an intelligent system consisting of many computer/sensor systems on wheels. These intelligent implements are seeking to identify weed vs crop and even varieties of weed. They can therefore enable ultraprecision site-specific action.

This trend can however a major long-term consequence for agrochemical companies, slowly changing their business from the supply of a single blockbuster volume chemical towards the supply of many niche specialized chemicals. In other words, it can change them into speciality chemical suppliers.

There are countless other examples that we will not consider here. We, however, refer to our report New Robotics and Drones 2018-2038: Technologies, Forecasts, Players for a deeper understanding of these emerging trends. This report is thus unique in its focus on key transformations in the world of robots and drones, and also in its depth and breadth. In this report, we have analysed more than 46 robotic and drone categories. We have developed technology roadmaps and 20-year segment-by-segment market forecasts in units and value. We have also identified and profiled the key players and innovators working in each sector.