The robotic industry is looking for the next big opportunity that could one day rival the automotive sector in size. It may have found its answer in the logistic and material handling sector.

The IDTechEx report Mobile Robots and Drones in Material Handling and Logistics 2018-2038 focuses on all mobile robots and drones in this sector. It also provides technology roadmaps and twenty-year market forecasts, in unit numbers and revenue, for 12 technologies: automated guided vehicles and carts (AGVs and AGCs); autonomous mobile vehicles and carts/units; mobile picking robots; last mile delivery ground robots (droids) and drones; and autonomous trucks and light delivery vans (level 4 and level 5 automation).

In this article we will focus on the use of mobile robots in automating the goods-to-person step in logistics and material handling.

AMRs will devour AGVs and AGCs?

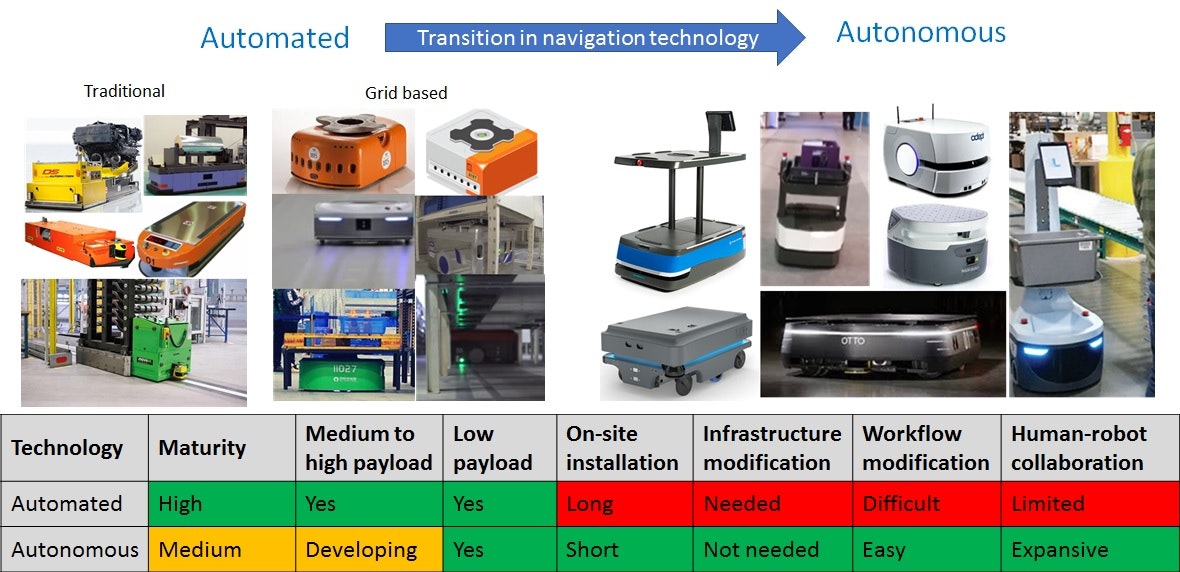

Traditional automated guided vehicles and carts (AGVs and AGCs) are a familiar sight in many facilities around the world. They act as distributed conveyer belt systems, carrying items along well-defined paths.

Depending on the specific navigation technology, this path can be marked by magnetic tape, conductive wires, reflective strips and so on. These AGVs and AGCs work well and are trusted to handle all manners of payload sizes ranging from a few Kg to several tonnes.

Their work flow is, however, fixed and thus hard to modify. The on-site installation time is often long and the scope for flexible human-robot collaboration is limited.

The next generation of this mobile automation will be based on AMRs (autonomous mobile robots). These AMRs have infrastructure independent navigation. They have the intelligence and the on-board sensor suite to learn (or be taught) to navigate a known semi-structured environment.

They are a less mature technology than traditional AGVs and AGVS and are intrinsically more risk prone given that their workflow is more flexible. It is this flexibility however that helps it overcome the limitations of traditional AGV/AGCs: their or their fleet's workflow can be easily modified and updated, human-robot collaboration in shared work spaces can be enabled and on-site installation times can be minimized.

These AMRs in logistic and material handling are now the focus of many exciting start-ups. The AMRs in this arena are in fact just one manifestation of the greater trend towards AMRs. Today, AMRs are being actively proposed (and trialled and even ordered in notable numbers) for use in security, cleaning, retail, hospitality, and numerous other sectors.

A transition will take place from automated towards autonomous vehicles and carts in warehouses and logistics. For more information see Mobile Robots and Drones in Material Handling and Logistics 2018-2038. Source: IDTechEx Research. Images are, in no particular order, from Kiva (Amazon), Geek+, Flashold, GreyOrange, Scallog, Swisslog, Otto, Adept, MiR, Locus Robotics, Fetch Robotics, 6 River systems, DS Automation, AGVE, m Daifuku, Autocraft, etc.

Today, our assessment is that the hardware part of the AMR is still an integral part of the software. As such, the AMR companies are mostly vertically integrated: they pick their components and assemble them (or have them assembled to their specification), and develop their software around the peculiarities of their hardware.

In the future, however, we foresee that the hardware will become modular and mass-manufactured. It will, as such, likely become commoditized. It can therefore follow the commercial trajectory that consumer (and now prosumer and professional) drones followed: DJI commoditized the hardware platform business through its aggressive pricing.

The software scene too will also undergo changes. Today, companies use RoS (with ample customization) to develop their specific software and UI suite. In the future, it is likely that common platforms will emerge to provide basic universal functions needed by AMRs.

There, however, will remain extensive ongoing opportunities in the software space. This is because the application (end use) space is fragmented. This means that AMRs will need to be customized to work in specific circumstances. As such, customer closeness and know-how will be a source of ongoing value even if some of the specialized functions shift to dominant cloud-based SaaS companies.

Those closest to the customer will also have ongoing opportunity to experiment with their models: they can provide their robots as a service or try out new added-value services. The former can ease uptake for the customer by making spent on robots part of operational costs like the wage bill. The latter can enable these providers to maintain a robust data loop in their operations. This data loop will enable them to offer higher-value-add analytics services to their customers and to stay ahead of the competition by iterating and optimising their products faster.

This type of emerging business scene- a hybrid of commoditized parts and software plus customized additional services- will create the foundation for the establishment of many interesting partnerships.

The automation of goods-to-person in logistics and material handling is here to stay and grow. Our report provides short-term as well as long-term segmented market projects (2018 to 2038). It finds that traditional AGV/AGCs will remain a stable business in the short term but will then tend towards obsolescence. This obsolescence will however in fact be about the technology merging into AMRs since infrastructure-independent navigation cover the traditional capabilities of AGV/AGVs whilst offering more flexibility and scope for human-robot collaboration.

Our report finds, however, that one version of AGCs that will retain and expand its use case: grid-based AGCs operating robot-only zones in warehouses. These are becoming popular with warehouses serving e-commerce markets. These AGCs rapidly shuttle totes around the facility to bring them to a human-staffed picking/packing station. They are excellent (highly productive) at automating the particular goods-to-person task.

The army of AGCs are controlled by a fleet and inventory management software system in which much of the value-add resides. The suppliers of such technology (hardware together with the appropriate software/UI) have proliferated globally to help fill the gap that was left when Kiva was acquired and taken off the market.

Mobile Robots and Drones in Material Handling and Logistics 2018-2038 provides a comprehensive assessment of this emerging trend. It is essential reading if you are interested, or affected, by the opportunities and threats that these technological and commercial changes will generate. This report will identify and profile the key players in these fields, will analyse the emerging technology landscape, will assess the business landscape by looking at various indicators such as annual investment levels, and will provide detailed supported short and long term (until 2038) market projects in value and unit numbers.